Playing with TRIS – the impact on middle-Australia

- On 13/05/2016

- TRIS, TTR

The Government’s Budget proposal to strip the tax exemption from earnings of assets backing Transition to Retirement Income Streams (TRIS) pensions may have a wider impact than initially realised.

The Government’s Budget proposal to strip the tax exemption from earnings of assets backing Transition to Retirement Income Streams (TRIS) pensions may have a wider impact than initially realised.

Under the proposal, earnings of assets supporting TRIS pensions will be taxed from July next year at the standard superannuation tax rate applying to the accumulation phase.

This change may impact on the ability of many middle-income Australian to catch up on superannuation provision in the final years of the working lives.

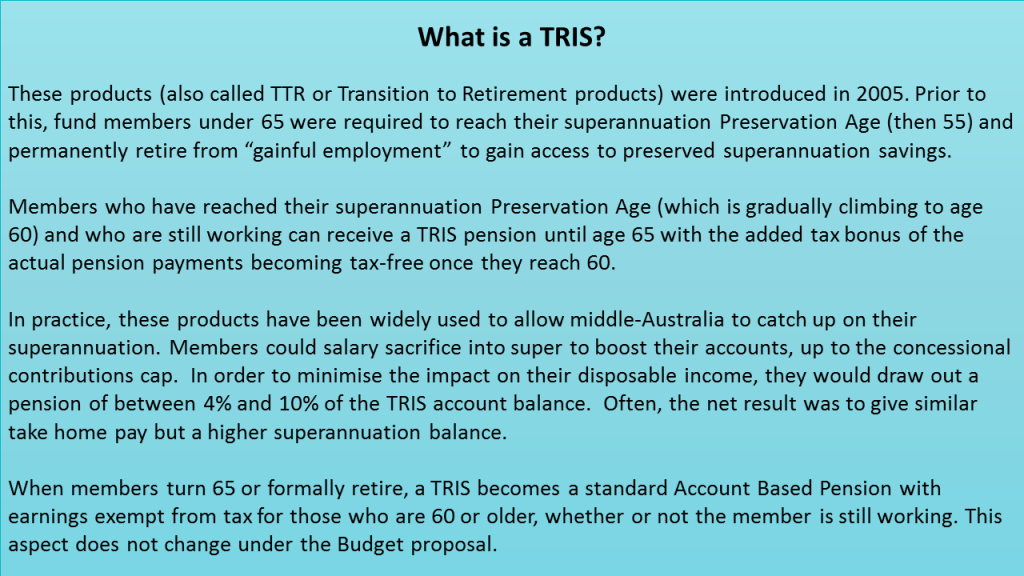

Who holds these products?

This change will hit more than the Government’s apparent target of wealthier, big-balance fund members. Rice Warner estimates that members hold 580,000 TRIS accounts supported by at least $40 billion in superannuation assets, as at June last year. About half the money is held in SMSF accounts.

The average balance of $69,000 is a modest average balance given that members receiving TRIS pensions are aged 56-64, with many holding the bulk of their super savings in pensions to maximise the current tax exemption.

The advantages

A key benefit of a TRIS is the tax exemption on earnings of assets backing the pension. Someone with a large superannuation balance can benefit from a TRIS as they remove the accumulation tax on earnings.

A popular strategy for wealthier fund members has been to recontribute at least part of their TRIS pension back into super as non-concessional (after-tax) contributions to boost their retirement savings and to minimise tax payable on death should the benefit be paid to non-dependent beneficiaries.

If they are over 60 and have more than $1.8 million in the TRIS, they have been able to draw $180,000 tax free and then re-contribute it as a non-concessional contribution.

This has allowed them to effectively grow their superannuation tax free and minimise potential taxes of non-dependent beneficiaries (such as their grown-up children) while they continue to work.

The Budget changes

In short, the Government proposes in the Budget to retain the transition-to-retirement pension but wants to remove their tax-free treatment.

It has also clobbered re-contribution strategies as these count towards the non-concessional lifetime cap of $500,000. In fact, the cap includes past re-contributed amounts even if these have just been recycling money for death tax minimisation.

One reason why some members will not establish a TRIS in future is that the Government proposes from July next year to remove the ability for members to elect to treat certain TRIS payments as lump sums. This had meant that the first $195,000 of the taxable component could be withdrawn tax-free.

Decisions to retire

No doubt, some fund members under 65 receiving TRIS pensions may decide to retire in order to retain the tax exemption on earnings from their pension assets. By retiring, a member would have met the two conditions for release, namely reaching the Preservation Age and retirement.

Members who are currently working part-time can obviously make a decision at any time to retire.

Fund trustees are required to be reasonably satisfied that a member intends never to be “gainfully” employed or self-employed again for payment on a full-time or part-time basis (at least ten hours a week). Inevitably, some retirees will later change their mind and return to work.

Short-term opportunity

Some fund members still in the workforce who had been considering taking a TRIS pension will no doubt decide to proceed given that the Government proposes not to remove the tax exemption until July next year. It will give a brief period to benefit from tax-free earnings.

TTR strategies may still appeal to some members who can use income from TRIS products to finance concessional contributions which would not otherwise be feasible, and benefit from differences between their marginal rate and the contributions tax rate. (For most middle-income earners, the contribution tax rate will still be 15% and their marginal income tax rate will be significantly higher.) However, the removal of the tax-free status of the assets backing the TRIS can dilute the overall tax benefits, and make decisions more difficult.

Another group of people who will continue to use a TRIS if the Government’s proposal becomes law are those who really use the pension income to transition into retirement. Typically, these members move from full to part-time work (whether by choice or out of necessity), using the pension income to help maintain their lifestyle as they approach full retirement.

Move back to accumulation

Many members currently receiving TRIS pensions will decide to move all their superannuation back into the accumulation phase so their fund will no longer have to make the minimum pension withdrawals each year. Some will decide to sell selected assets in the tax-free pension phase before shifting back to an accumulation fund. This will be done to remove any accrued CGT which might be paid in the accumulation account.

Among the clear winners from this Budget are the specialist financial superannuation advisers whose guidance should be in high demand – including in regard to TRIS pensions. Those who do not feel that they can afford this advice, and are not in a position to understand an increasingly complex system for themselves, may find that their retirement outcomes fall well short of what they could have achieved.

0 Comments